Tech

Crypto politics are already reshaping the 2024 elections.

After the spectacular fall of FTX CEO Sam Bankman-Fried, you might have expected the embattled cryptocurrency sector, and its sophisticated lobbying operations, to have ground to a halt. But if anything, both are back with a vengeance—and the regulatory post-SBF crackdown that followed has spurred the sector to potentially become a major political force in 2024.

A new, unholy alliance has emerged on Capitol Hill, and it’s hoping not just to recraft governmental policy around digital funny money but to push its antiregulatory agenda across a whole host of elections. To do so, the crypto industry is teaming up with the people behind the latest megahyped, bubblicious tech trend: the artificial intelligence boom.

You may already have noticed crypto and tech money swishing around in the 2024 primaries. For the open California Senate seat, crypto-backed super PAC Fairshake splurged $10 million on ads against candidate Katie Porter, whose progressivism and crypto skepticism made her an enemy of the industry. She, of course, would lose. An affiliated PAC, Defend American Jobs, likewise dove into North Carolina’s GOP primaries, throwing half a million to the winning candidate for the 14th Congressional District. That PAC also contributed $3 million on behalf of West Virginia Gov. Jim Justice, who’s far and away the front-runner in his Senate primary and will inevitably succeed Sen. Joe Manchin come 2025.

Another Fairshake affiliate, Protect Progress, has put millions behind candidates who have explicitly expressed their support for the crypto industry. The group blew nearly $2 million to boost Shomari Figures in the Democratic primary for Alabama’s 2nd Congressional District; he ended up winning the April 16 runoff by 22 points. Protect Progress also spent nearly $1 million in support of Julie Johnson, who crushed her opponents in the Dem primary for Texas’ 32nd Congressional District. The competitive primaries of crypto-supporting Democratic Maryland Senate candidates David Trone and Angela Ashbrook have seen a large influx of money from obscurely named crypto PACs like Defend American Jobs.

It’s in not just the electoral sphere but also the messaging being sent directly to current officials. According to CNBC, a dark-money nonprofit called the Cedar Innovation Foundation “is being heavily funded by crypto industry players” and running ads encouraging crypto enthusiasts to request that Ohio Sen. Sherrod Brown loudly oppose Securities and Exchange Commission Chair Gary Gensler; both are considered villains in the crypto world, along with Sens. Elizabeth Warren and Roger Marshall, who’ve likewise been the target of Cedar Innovation ads thanks to their co-sponsorship of the hated Digital Asset Anti–Money Laundering Act. Warren has also been courted by individual blockchain workers hoping to dissuade her from that legislation, and received a letter co-signed by figures from big firms—Coinbase, Andreessen Horowitz, the Blockchain Association—asking the same. A Fairshake spokesperson told Bloomberg that crypto donors will likely be homing in next on the primaries in important states like Michigan and Montana.

To see how we got here, despite all of crypto’s recent travails, it’s worth looking back to the first significant surge in crypto lobbying that occurred throughout 2021, when all aspects of the industry (Bitcoin, alternative currencies, NFTs, the blockchain) gained mainstream exposure, political acceptance, and frenzied valuations as a result of lockdown-fueled interest in virtual economics and get-rich-quick schemes. The then-nascent Biden administration had already turned its attention to crypto regulation, with the SEC lodging its securities charges against Ripple in February of that year—while also approving crypto exchange Coinbase’s request to go public. One of that company’s biggest investors, famed venture capital firm Andreessen Horowitz, lavished its money on other crypto players and launched an aggressive lobbying operation to shield the industry from regulations around tax reporting and money laundering—and, most importantly, to exclude it from SEC oversight. Results came quickly: Prior to its November passage, Biden’s infrastructure bill contained expansive tax-reporting requirements for Bitcoin miners that were significantly weakened by aggressive lobbying (including by Coinbase itself).

The point was to persuade both Biden administration members and members of Congress—from either party—to embrace crypto monkeymakers’ relevant legislative agenda. The clearest examples of this success manifested with Sens. Kirsten Gillibrand and Cynthia Lummis, who were wined and dined by several crypto bigwigs—Grayscale, the Blockchain Association, the Chamber of Digital Commerce, BTC Inc.—and introduced a bill, in the midst of the summer 2022 crypto crashes, that would have achieved lobbyists’ goals of shifting governance away from the SEC and exempting digital assets from certain tax requirements, like capital gains. Other senators who earned cash from SBF put forth a more constrictive bill that likewise placed crypto under the oversight of the Commodity Futures Trading Commission. Congressional representatives who earned the benefits of crypto-lobby largesse, like Republican Patrick McHenry, also gravitated thus.

Then, after FTX’s late-2022 collapse drew additional scrutiny to all the pols who glad-handed with SBF, the enthusiasm for crypto-industry handouts duly subsided. The entire industry, already smarting from the impact of interest rate hikes and the misdeeds of companies (and eager lobbyists) like Terraform Labs and Celsius, seemed ready to back off for a bit, as was made apparent by the 2023 Super Bowl’s conspicuous dearth of crypto ads.

Since the collapse of the FTX empire, the Biden administration has gone after every major crypto firm in existence, notching some significant legal victories along the way—for example, Binance, once the world’s largest crypto exchange, has had its business absolutely crushed by U.S. and international prosecution. (Its former CEO, Changpeng Zhao, was forced to step away from both the company and crypto altogether and just earned a four-month prison sentence.) Just one day after it lodged its own Binance suit, the SEC also sued Coinbase, the largest crypto exchange based in the U.S., for allegedly acting as an unregistered securities institution—a suit that, if successful, could tank Coinbase’s business model for good.

That’s a key sticking point in this fight: the government’s attempt to define many non-Bitcoin currencies, such as Solana, as securities that should be governed as such—not commodities, as Bitcoin is considered thanks to its collective use as a store of value, rather than a proper investment contract and vehicle (which is how securities function).

As the government lawsuits around these classifications began flying in, companies like Coinbase and orgs like the Blockchain Association escalated their lobbying game, playing nice by sweet-talking all manner of lawmakers into re-upping support for their preferred legislation (i.e., stripping the SEC of crypto-governance authority and granting states oversight over dollar-pegged tokens). Coinbase even launched a grassroots advocacy nonprofit called the Stand With Crypto Alliance, which partnered with prominent companies like Gemini and Blockchain.com, organized retail crypto traders to show their support, and produced a bunch of advocacy ads.

In December, three long-shot presidential candidates—Republicans Vivek Ramaswamy and Asa Hutchinson, plus Democrat Dean Phillips—gathered for an event hosted by Stand With Crypto, during which they expressed their support for the industry and promised to reduce aggressive government oversight. None of those guys got too far, of course, but their shared stance was telling as to what crypto lobbyists did expect from other politicians: Potential spoiler Robert F. Kennedy Jr., who has been backed by prominent crypto advocates like former Overstock.com CEO Patrick Byrne, spoke at the 2023 Bitcoin Conference in Miami, and recently proclaimed at a Michigan rally that he would “put the entire U.S. budget on blockchain.” (For whatever it’s worth, even city-level efforts to put certain municipal functions on the blockchain haven’t turned out so great.) Naturally, RFK Jr. has a high candidate rating from Stand With Crypto.

After the Republican-led House Financial Services Committee approved the preferred bills, Stand With Crypto kept bugging Congress to pass the legislation in full and advocated strongly for the crypto-friendly Republican Tom Emmer to replace Kevin McCarthy as House speaker. But that push failed, and the bills fell by the wayside, not least because they faced doubts from skeptical Democrats—including and especially Brown, who has been heading the Senate Banking Committee since 2021. Even an attempt at passing crypto provisions within the defense budget was scuttled. The crypto lobby ended 2023 with a record-breaking spend and little to show for it.

But a pair of court rulings last summer helped crypto companies successfully beat certain charges brought by the SEC. First, the SEC’s suit against Ripple, on which a federal judge ruled that the trading protocol’s sale of its XRP token straight to investors met the definition of a securities transaction—but trades of XRP between investors on a secondary market did not constitute trading in securities. The SEC’s request for an immediate appeal was rejected, although the judge did note that her ruling should not weigh on all digital assets swapped on secondary markets; rather, her legal definition was limited to XRP and XRP alone, leaving a hazy space for the overall altcoins-are-securities argument. And the SEC lost an appeal against the company Grayscale, after an appellate judgment established that the crypto firm could incorporate Bitcoin into a spot exchange-traded fund, essentially allowing investors to trade a security whose financial health has a stake in Bitcoin’s price. The court-mandated SEC approval of several spot Bitcoin ETFs in January is credited with fueling the remarkable comeback (and record heights) Bitcoin’s value has achieved since its 2022 nadir, even as that surge has fallen just a touch.

Another seed of the crypto lobby’s comeback was planted just weeks after SBF’s downfall: the launch of ChatGPT. As the impressive chatbot became one of the fastest-growing apps ever, crypto bros and their financiers noticed the rapid consumer and professional adoption of the technology and realized they had a shot at a natural alliance. The CEO of ChatGPT’s parent company, OpenAI, was also a crypto enthusiast with a stake in the Andreessen Horowitz–backed biometric-crypto project WorldCoin.

Burgeoning A.I. startups and companies also needed massive amounts of infrastructure to handle their resource-intensive tech—and stranded crypto miners had a lot of that lying around, including data centers and cooling systems and energy hookups that companies needed if they wanted to catch up to OpenAI’s progress. Financially hurting digital-asset specialists figured out they could ride investment hype around A.I. by incorporating the tech into crypto processes, and these so-called A.I. tokens have certainly skyrocketed in value, much like every other company having anything to do with A.I. these days. And, hey, SBF’s A.I. investments had turned out to be his single smartest decisions.

But beyond material interests, crypto die-hards and A.I. bulls share something even more essential: a hunger for uninhibited growth and an allergy to regulatory burdens.

You may recall that late last year, OpenAI CEO Sam Altman was briefly ousted from his company after the board expressed its displeasure with Altman’s decisionmaking. This provoked a revolt within OpenAI and among the broader tech world, which perceived Altman’s firing as an unforgivable trespass from A.I. insiders who wished to be more careful, rather than hasty, in developing their tools.

Such “doomers” typically adhered to the philosophies of effective altruism and longtermism, whose followers (including SBF) dedicated themselves to minimizing any risks to human flourishing—including that of runaway, superintelligent A.I. But a rival faction, carrying the mocking banner of effective accelerationism, viewed any and all slowdown in A.I. development as existentially dangerous to the mission of furthering life-changing A.I. that could bring humanity toward new frontiers (and could make its practitioners a lotta money).

Such accelerationists viewed SBF’s criminality as a discredit to effective altruism and marched to the tune of Marc Andreessen’s “Techno-Optimist Manifesto,” which cheered on unimpeded development of all technology—no government interference or regulation, no “doomers” with doubts about efficacy or considerations of social justice, no guardrails around safety. Just let ’em cook, as the kids say. (Andreessen Horowitz has, of course, poured millions upon millions into A.I. as its investments into other ventures have flopped.)

The boldest Bitcoin and crypto advocates, including Coinbase’s Brian Armstrong, have glommed on to this philosophy. And it has changed the way they lobby too.

For one, there’s been a sharp turn to the right. Previous crypto-lobby efforts may have heavily courted both sides of the aisle, but the outrage at the Biden administration’s crypto crackdowns and meekest attempts at crafting A.I. guidelines make it clear that techies desire a wholesale change—one more libertarian and generally hands-off, and one less apt to work with non-centrist Democrats than the effective-altruist A.I. advisers currently dominating (and still lobbying) Washington.

Nitish Pahwa

I Was There When Sam Bankman-Fried Was Found Guilty. I Think I Know Why He Did It.

Read More

Around the same time Coinbase started Stand With Crypto, Armstrong announced that he and his business would be donating to the super PAC Fairshake, which would subsequently launch ads supporting the Republican co-sponsors of Armstrong’s dream House bills (including McHenry, even though he is not seeking reelection).

Fairshake also launched the PACs Protect Progress and Defend American Jobs, and the three share common donors, including Coinbase, Andreessen Horowitz, and Ripple. Notably, per CNBC, rumors have it that Coinbase will also donate to the Cedar Innovation Foundation, the dark-money nonprofit spending against Sens. Brown and Warren (the latter of whom is also facing a long-shot challenge from Republican John Deaton, a former crypto lawyer enjoying a lot of backing from that industry as well as arguing on Coinbase’s behalf before the SEC). Coinbase has also notched some powerful political allies, including former Los Angeles Mayor Antonio Villaraigosa, who recently came on to help advise the firm.

It’s also worth noting that Cedar Innovation has hired a longtime lobbying firm, Mindset Advocacy, whose staffer Charlie Schreiber will be tasked with persuading his old boss McHenry to drop his long-pursued stablecoins bill. (It’s likely this is the reason McHenry has earned Fairshake money, in spite of his pending retirement.)

All these efforts are receiving ample help from crypto-and-A.I. cheerleaders. Bullish VCs like Fred Wilson, Ron Conway (who raged against Altman’s ouster), and Marc Andreessen have all been chipping in for Fairshake. According to Puck News’ Theodore Schleifer, Andreessen is going even further by once again donating to crypto champions like Gillibrand and Lummis, and his firm dropped ample funds on a different crypto dark-money operation, Digital Innovation for America, which is aligned with a Republican consulting firm that has splurged on behalf of multiple candidates—like Emmer and California Rep. Young Kim—who’ve earned the crypto stamp of approval.

You have to take Andreessen & Co. only at their word to understand why they’re going all in on this crusade. In line with his VC partner’s techno-optimist manifesto, Ben Horowitz wrote a December blog post that denounced “misguided and politicized regulation,” decried lobbyists who are “often at odds with a positive technological future,” and announced that the firm would pursue its political interests thus: “If a candidate supports an optimistic technology-enabled future, we are for them. If they want to choke off important technologies, we are against them.” Those “important technologies,” naturally, include both A.I. and “decentralized technologies from the blockchain/crypto/web3 ecosystem.”

-

The Meltdown in Michigan Says It All About Where MAGA Is Headed

-

When Stormy Daniels Told Her Story in Court, the Absurd Horror of This Trial Finally Hit Home

-

Donald Trump Really Did This to Himself

-

Donald Trump’s Lawyer Helped Make Alvin Bragg’s Case for Him

And in case it isn’t clear what the endgame is, just look at what that ecosystem is currently up to in the judicial field. The Crypto Freedom Alliance of Texas is an industry group from a crypto-friendly state that formed in September with backing from—who else?—Coinbase and Andreessen Horowitz. In February, it lodged a lawsuit against the SEC in the administration-hostile 5th Circuit, challenging its authority to regulate crypto transactions.

The 5th Circuit has already all but declared the SEC to be unconstitutional in a case that has traveled up to the Supreme Court, which seems ready to curtail much of the administrative state’s law-enforcement power. The setup of the Crypto Freedom Alliance suit, and its choice of litigators, makes clear that the plaintiff wants to further weaken the SEC.

Add that to the Big Tech firms currently attempting to argue in court that the Federal Trade Commission and the National Labor Relations Board are also unconstitutional, and it becomes apparent that tech firms plan to secure a “positive future” by not just sweet-talking the political system but gutting its power altogether.

Correction, May 2, 2024: This article originally misstated that the SEC’s suit against Ripple was rejected on appeal. The judge denied the SEC permission to file an interlocutory appeal.

Tech

Harvard Alumni, Tech Moguls, and Best-Selling Authors Drive Nearly $600 Million in Pre-Order Sales

BlockDAG Network’s history is one of innovation, perseverance, and a vision to push the boundaries of blockchain technology. With Harvard alumni, tech moguls, and best-selling authors at the helm, BlockDAG is rewriting the rules of the cryptocurrency game.

CEO Antony Turner, inspired by the successes and shortcomings of Bitcoin and Ethereum, says, “BlockDAG leverages existing technology to push the boundaries of speed, security, and decentralization.” This powerhouse team has led a staggering 1,600% price increase in 20 pre-sale rounds, raising over $63.9 million. The secret? Unparalleled expertise and a bold vision for the future of blockchain.

Let’s dive into BlockDAG’s success story and find out what the future holds for this cryptocurrency.

The Origin: Why BlockDAG Was Created

In a recent interview, BlockDAG CEO Antony Turner perfectly summed up why the market needs BlockDAG’s ongoing revolution. He said:

“The creation of BlockDAG was inspired by Bitcoin and Ethereum, their successes and their shortcomings.

If you look at almost any new technology, it is very rare that the first movers remain at the forefront forever. Later incumbents have a huge advantage in entering a market where the need has been established and the technology is no longer cutting edge.

BlockDAG has done just that: our innovation is incorporating existing technology to provide a better solution, allowing us to push the boundaries of speed, security, and decentralization.”

The Present: How Far Has BlockDAG Come?

BlockDAG’s presale is setting new benchmarks in the cryptocurrency investment landscape. With a stunning 1600% price increase over 20 presale lots, it has already raised over $63.9 million in capital, having sold over 12.43 billion BDAG coins.

This impressive performance underscores the overwhelming confidence of investors in BlockDAG’s vision and leadership. The presale attracted over 20,000 individual investors, with the BlockDAG community growing exponentially by the hour.

These monumental milestones have been achieved thanks to the unparalleled skills, experience and expertise of BlockDAG’s management team:

Antony Turner – Chief Executive Officer

Antony Turner, CEO of BlockDAG, has over 20 years of experience in the Fintech, EdTech, Travel and Crypto industries. He has held senior roles at SPIRIT Blockchain Capital and co-founded Axona-Analytics and SwissOne. Antony excels in financial modeling, business management and scaling growth companies, with expertise in trading, software, IoT, blockchain and cryptocurrency.

Director of Communications

Youssef Khaoulaj, CSO of BlockDAG, is a Smart Contract Auditor, Metaverse Expert, and Red Team Hacker. He ensures system security and disaster preparedness, and advises senior management on security issues.

advisory Committee

Steven Clarke-Martin, a technologist and consultant, excels in enterprise technology, startups, and blockchain, with a focus on DAOs and smart contracts. Maurice Herlihy, a Harvard and MIT graduate, is an award-winning computer scientist at Brown University, with experience in distributed computing and consulting roles, most notably at Algorand.

The Future: Becoming the Cryptocurrency with the Highest Market Cap in the World

Given its impressive track record and a team of geniuses working tirelessly behind the scenes, BlockDAG is quickly approaching the $600 million pre-sale milestone. This crypto powerhouse will soon enter the top 30 cryptocurrencies by market cap.

Currently trading at $0.017 per coin, BlockDAG is expected to hit $1 million in the coming months, with the potential to hit $30 per coin by 2030. Early investors have already enjoyed a 1600% ROI by batch 21, fueling a huge amount of excitement around BlockDAG’s presale. The platform is seeing significant whale buying, and demand is so high that batch 21 is almost sold out. The upcoming batch is expected to drive prices even higher.

Invest in BlockDAG Pre-Sale Now:

Pre-sale: https://purchase.blockdag.network

Website: https://blockdag.network

Telegram: https://t.me/blockDAGnetwork

Discord: Italian: https://discord.gg/Q7BxghMVyu

No spam, no lies, just insights. You can unsubscribe at any time.

- Space and Time uses zero-knowledge proofs to ensure secure and tamper-proof data processing for smart contracts and enterprises.

- The integration facilitates faster development and deployment of Distributed Secure Services (DSS) on the Karak platform.

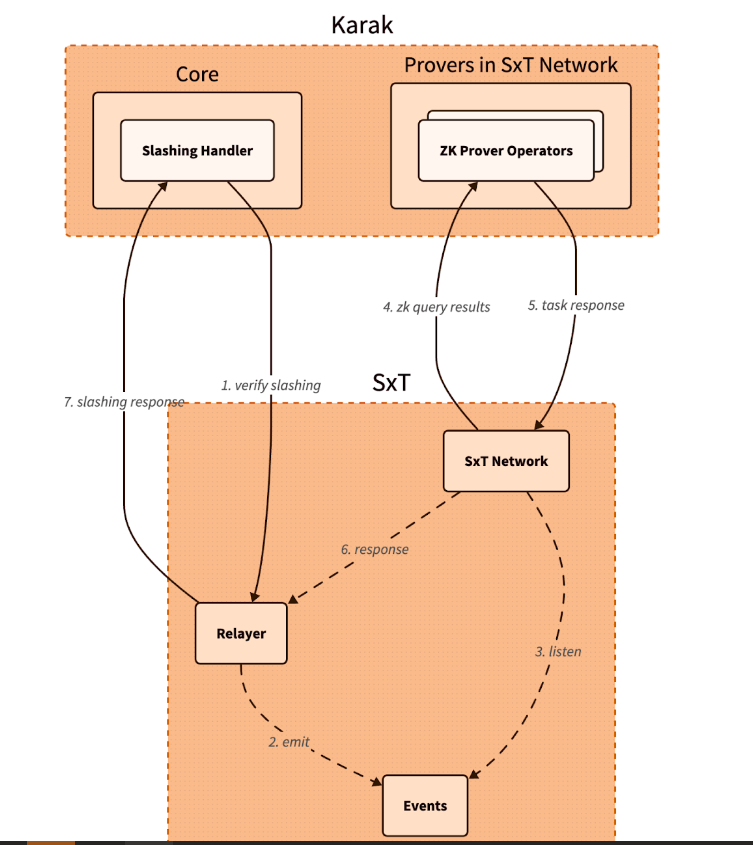

Karak, a platform known for its strong security capabilities, is enhancing its Distributed Secure Services (DSS) by integrating Space and Time as a zero-knowledge (ZK) coprocessor. This move is intended to strengthen trustless operations across its network, especially in slashing and rewards mechanisms.

Space and Time is a verifiable processing layer that uses zero-knowledge proofs to ensure that computations on decentralized data warehouses are secure and untampered with. This system enables smart contracts, large language models (LLMs), and enterprises to process data without integrity concerns.

The integration with Karak will enable the platform to use Proof of SQL, a new ZK-proof approach developed by Space and Time, to confirm that SQL query results are accurate and have not been tampered with.

One of the key features of this integration is the enhancement of DSS on Karak. DSS are decentralized services that use re-staked assets to secure the various operations they provide, from simple utilities to complex marketplaces. The addition of Space and Time technology enables faster development and deployment of these services, especially by simplifying slashing logic, which is critical to maintaining security and trust in decentralized networks.

Additionally, Space and Time is developing its own DSS for blockchain data indexing. This service will allow community members to easily participate in the network by running indexing nodes. This is especially beneficial for applications that require high security and decentralization, such as decentralized data indexing.

The integration architecture follows a detailed and secure flow. When a Karak slashing contract needs to verify a SQL query, it calls the Space and Time relayer contract with the required SQL statement. This contract then emits an event with the query details, which is detected by operators in the Space and Time network.

These operators, responsible for indexing and monitoring DSS activities, validate the event and route the work to a verification operator who runs the query and generates the necessary ZK proof.

The result, along with a cryptographic commitment on the queried data, is sent to the relayer contract, which verifies and returns the data to the Karak cutter contract. This end-to-end process ensures that the data used in decision-making, such as determining penalties within the DSS, is accurate and reliable.

Karak’s mission is to provide universal security, but it also extends the capabilities of Space and Time to support multiple DSSs with their data indexing needs. As these technologies evolve, they are set to redefine the secure, decentralized computing landscape, making it more accessible and efficient for developers and enterprises alike. This integration represents a significant step towards a more secure and verifiable digital infrastructure in the blockchain space.

Website | X (Twitter) | Discord | Telegram

No spam, no lies, just insights. You can unsubscribe at any time.

Iconic Italian luxury carmaker Ferrari has announced the expansion of its cryptocurrency payment system to its European dealer network.

The move, which follows a successful launch in North America less than a year ago, raises a crucial question for CFOs across industries: Is it time to consider accepting cryptocurrency as a form of payment for your business?

Ferrari’s move isn’t an isolated one. It’s part of a broader trend of companies embracing digital assets. As of 2024, we’re seeing a growing number of companies, from tech giants to traditional retailers, accepting cryptocurrencies.

This change is determined by several factors:

- Growing mainstream adoption of cryptocurrencies

- Growing demand from tech-savvy and affluent consumers

- Potential for faster and cheaper international transactions

- Desire to project an innovative brand image

Ferrari’s approach is particularly noteworthy. They have partnered with BitPay, a leading cryptocurrency payment processor, to allow customers to purchase vehicles using Bitcoin, Ethereum, and USDC. This satisfies their tech-savvy and affluent customer base, many of whom have large digital asset holdings.

Navigating Opportunities and Challenges

Ferrari’s adoption of cryptocurrency payments illustrates several key opportunities for companies considering this move. First, it opens the door to new customer segments. By accepting cryptocurrency, Ferrari is targeting a younger, tech-savvy demographic—people who have embraced digital assets and see them as a legitimate form of value exchange. This strategy allows the company to connect with a new generation of affluent customers who may prefer to conduct high-value transactions in cryptocurrency.

Second, cryptocurrency adoption increases global reach. International payments, which can be complex and time-consuming with traditional methods, become significantly easier with cryptocurrency transactions. This can be especially beneficial for businesses that operate in multiple countries or deal with international customers, as it potentially reduces friction in cross-border transactions.

Third, accepting cryptocurrency positions a company as innovative and forward-thinking. In today’s fast-paced business environment, being seen as an early adopter of emerging technologies can significantly boost a brand’s image. Ferrari’s move sends a clear message that they are at the forefront of financial innovation, which can appeal to customers who value cutting-edge approaches.

Finally, there is the potential for cost savings. Traditional payment methods, especially for international transactions, often incur substantial fees. Cryptocurrency transactions, on the other hand, can offer lower transaction costs. For high-value purchases, such as luxury cars, these savings could be significant for both the business and the customer.

While the opportunities are enticing, accepting cryptocurrency payments also presents significant challenges that businesses must address. The most notable of these is volatility. Cryptocurrency values can fluctuate dramatically, sometimes within hours, posing potential risk to businesses that accept them as payment. Ferrari addressed this challenge by implementing a system that instantly converts cryptocurrency received into traditional fiat currencies, effectively mitigating the risk of value fluctuations.

Regulatory uncertainty is another major concern. The legal landscape surrounding cryptocurrencies is still evolving in many jurisdictions around the world. This lack of clear and consistent regulations can create compliance challenges for companies, especially those operating internationally. Companies must remain vigilant and adaptable as new laws and regulations emerge, which can be a resource-intensive process.

Implementation costs are also a significant obstacle. Integrating cryptocurrency payment systems often requires substantial investment in new technology infrastructure and extensive staff training. This can be especially challenging for small businesses or those with limited IT resources. The costs are not just financial; a significant investment of time is also required to ensure smooth implementation and operation.

Finally, security concerns loom large in the world of cryptocurrency transactions. While blockchain technology offers some security benefits, cryptocurrency transactions still require robust cybersecurity measures to protect against fraud, hacks, and other malicious activity. Businesses must invest in robust security protocols and stay up-to-date on the latest threats and protections, adding another layer of complexity and potential costs to accepting cryptocurrency payments.

Strategic Considerations for CFOs

If you’re thinking of following in Ferrari’s footsteps, here are the key factors to consider:

- Risk Assessment: Carefully evaluate potential risks to your business, including financial, regulatory, and reputational risks.

- Market Analysis: Evaluate whether your customer base is significantly interested in using cryptocurrencies for payments.

- Technology Infrastructure: Determine the costs and complexities of implementing a cryptographic payment system that integrates with existing financial processes.

- Regulatory Compliance: Ensure that cryptocurrency acceptance is in line with local regulations in all markets you operate in. Ferrari’s gradual rollout demonstrates the importance of this consideration.

- Financial Impact: Analyze how accepting cryptocurrency could impact your cash flow, accounting practices, and financial reporting.

- Partnership Evaluation: Consider partnering with established crypto payment processors to reduce risk and simplify implementation.

- Employee Training: Plan comprehensive training to ensure your team is equipped to handle cryptocurrency transactions and answer customer questions.

While Ferrari’s adoption of cryptocurrency payments is exciting, it’s important to consider this trend carefully.

A CFO’s decision to adopt cryptocurrency as a means of payment should be based on a thorough analysis of your company’s specific needs, risk tolerance, and strategic goals. Cryptocurrency payments may not be right for every business, but for some, they could provide a competitive advantage in an increasingly digital marketplace.

Remember that the landscape is rapidly evolving. Stay informed about regulatory changes, technological advancements, and changing consumer preferences. Whether you decide to accelerate your crypto engines now or wait in the pit, keeping this payment option on your radar is critical to navigating the future of business transactions.

Was this article helpful?

Yes No

Sign up to receive your daily business insights

The world’s largest cryptocurrency, Bitcoin (BTC), suffered a significant price decline on Wednesday, falling below $65,000. The decline coincides with a broader market sell-off that has hit technology stocks hard.

Cryptocurrency Liquidations Hit Hard

CoinGlass data reveals a surge in long liquidations in the cryptocurrency market over the past 24 hours. These liquidations, totaling $220.7 million, represent forced selling of positions that had bet on price increases. Bitcoin itself accounted for $14.8 million in long liquidations.

Ethereum leads the decline

Ethereal (ETH), the second-largest cryptocurrency, has seen a steeper decline than Bitcoin, falling nearly 8% to trade around $3,177. This decline mirrors Bitcoin’s price action, suggesting a broader market correction.

Cryptocurrency market crash mirrors tech sector crash

The cryptocurrency market decline appears to be linked to the significant losses seen in the U.S. stock market on Wednesday. Stock market listing The index, heavily weighted toward technology stocks, posted its sharpest decline since October 2022, falling 3.65%.

Analysts cite multiple factors

Several factors may have contributed to the cryptocurrency market crash:

- Tech earnings are underwhelming: Earnings reports from tech giants like Alphabet are disappointing (Google(the parent company of), on Tuesday, triggered a sell-off in technology stocks with higher-than-expected capital expenditures that could have repercussions on the cryptocurrency market.

- Changing Political Landscape: The potential impact of the upcoming US elections and changes in Washington’s policy stance towards cryptocurrencies could influence investor sentiment.

- Ethereal ETF Hopes on the line: While bullish sentiment around a potential U.S. Ethereum ETF initially boosted the market, delays or rejections could dampen enthusiasm.

Analysts’ opinions differ

Despite the short-term losses, some analysts remain optimistic about Bitcoin’s long-term prospects. Singapore-based cryptocurrency trading firm QCP Capital believes Bitcoin could follow a similar trajectory to its post-ETF launch all-time high, with Ethereum potentially converging with its previous highs on sustained institutional interest.

Rich Dad Poor Dad Author’s Prediction

Robert Kiyosaki, author of the best-selling Rich Dad Poor Dad, predicts a potential surge in the price of Bitcoin if Donald Trump is re-elected as US president. He predicts a surge to $105,000 per coin by August 2025, fueled by a weaker dollar that is set to boost US exports.

BTC/USD Technical Outlook

Bitcoin price is currently trading below key support levels, including the $65,500 level and the 100 hourly moving average. A break below the $64,000 level could lead to further declines towards the $63,200 support zone. However, a recovery above the $65,500 level could trigger another increase in the coming sessions.

Lawrence Lepard: how the rates could break down the global economy – again!

Diddy’s collapse was no coincidence: Whitney Webb connects the points!

Because the last Bitcoin landfill was actually a false financial flag – Jeff Booth

Lyn Alden Finally forecast: Bitcoin set on SkyMate as Swing Markets

Omega Candle Alert! The market is about to explode with the bullish energy Samson Mow

Modiv Industrial to release Q2 2024 financial results on August 6

Volta Finance Limited – Director/PDMR Shareholding

Apple to report third-quarter earnings as Wall Street eyes China sales

Leeds hospitals trust says finances are “critical” amid £110m deficit

Inventiva reports 2024 First Quarter Financial Information¹ and provides a corporate update

Lawrence Lepard: how the rates could break down the global economy – again!

Diddy’s collapse was no coincidence: Whitney Webb connects the points!

Because the last Bitcoin landfill was actually a false financial flag – Jeff Booth

Lyn Alden Finally forecast: Bitcoin set on SkyMate as Swing Markets

Omega Candle Alert! The market is about to explode with the bullish energy Samson Mow

-

News9 months ago

News9 months agoModiv Industrial to release Q2 2024 financial results on August 6

-

News9 months ago

News9 months agoVolta Finance Limited – Director/PDMR Shareholding

-

News9 months ago

News9 months agoApple to report third-quarter earnings as Wall Street eyes China sales

-

News11 months ago

News11 months agoLeeds hospitals trust says finances are “critical” amid £110m deficit

-

News11 months ago

News11 months agoInventiva reports 2024 First Quarter Financial Information¹ and provides a corporate update

-

News9 months ago

News9 months agoNumber of Americans filing for unemployment benefits hits highest level in a year

-

DeFi11 months ago

DeFi11 months ago🏴☠️ Pump.Fun operated by Insider Exploit

-

Tech11 months ago

Tech11 months agoBitcoin’s Correlation With Tech Stocks Is At Its Highest Since August 2023: Bloomberg ⋆ ZyCrypto

-

Tech11 months ago

Tech11 months agoEverything you need to know

-

Videos11 months ago

Videos11 months ago“We will enter the ‘banana zone’ in 2 WEEKS! Cryptocurrency prices will quadruple!” – Raoul Pal

-

Markets11 months ago

Markets11 months agoWhale Investments in Bitcoin Hit $100 Billion in 2024, Fueling Insane Investor Optimism ⋆ ZyCrypto

-

Markets11 months ago

Markets11 months agoCrazy $3 Trillion XRP Market Cap Course Charted as Ripple CEO Calls XRP ETF “Inevitable” ⋆ ZyCrypto