Markets

BITO: Bitcoin Bear Market Begins As Excess Liquidity Dries Up (NYSEARCA:BITO)

Eoneren

One of the first articles I published this year was “BITO: 2024 May Be Bitcoin’s ‘Make Or Break’ Year.” At that time, I was bearish on the popular Bitcoin Strategy ETF (NYSEARCA:BITO) due to what I perceived as a potential top to the cryptocurrency bull market. I also believe that BITO’s risks were slightly elevated because of its exposure to liquidity risk factors in the Bitcoin futures market.

BITO has declined by ~10% since then, although its total return is positive due to its capital distribution. Bitcoin is still up 30% YTD but has lost around 17% of its value over the past month, with BITO falling by 23%. It is worth pointing out that I was not so bearish on BITO that I saw it as a short opportunity. As I stated,

I would not short Bitcoin or BITO because it could quickly rise higher over the coming months due to decent speculative momentum.

This view has primarily proven accurate. Bitcoin and BITO initially continued to climb over the spring months and have reversed those gains. That said, Bitcoin is still higher than when I became bearish on it. Thus, I think it is more reasonable to consider whether or not it may be a good time to short Bitcoin or BITO. Of course, other factors could still prove bullish for Bitcoin, so I aim to reconsider both the positive and negative arguments surrounding BITO to provide an updated outlook on the fund and its underlying asset.

Why Bitcoin and BITO Have Likely Peaked

My dominant view is that Bitcoin and most cryptocurrencies have reached a cyclical peak. It is worth stating outright that my views on Bitcoin are predicated on my fundamental belief that it is a speculative vehicle and not a viable currency. Those curious regarding my specific views may benefit from reading my recent article on the Bitcoin “miner” Riot Platforms (RIOT), “Riot Platforms: A Cash-Burning Machine, Even In The Crypto Bull Market.“

To summarize, I believe Bitcoin’s energy transaction cost and time length are magnitudes too high to make it remotely viable as a currency. That is not to say cryptocurrencies may not have viability, but that Bitcoin is likely akin to a dinosaur. It is based on a very outdated technological framework compared to more recent innovations like XRP or XMR that have superior transaction times and greater privacy abilities (particularly with XMR), as well as lack the extremely power-intensive platform such as used by Bitcoin miners like Riot. For example, while some of Texas is seeing its grid fail due to the hurricane, Riot may be using GW of power to mine an increasingly small amount of Bitcoin.

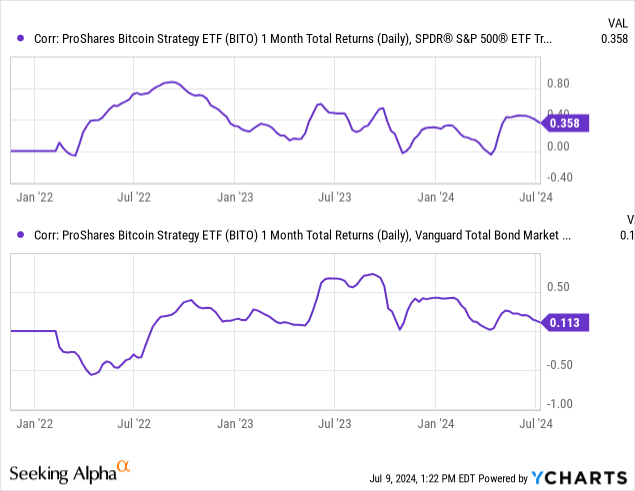

To me, issues such as that are potential catalysts that could lead to the gradual or rapid disbelief in Bitcoin. BITO is based on Bitcoin, which, in turn, is powered by speculative activity and, in my view, misfocused hope. Bitcoin and BITO are also poor hedges, with BITO being positively correlated to stocks and bonds based on monthly total returns of the S&P 500 ETF (SPY) and the Bond market ETF (BND). See below:

Many see Bitcoin and BITO as hedges against financial market risk. For the most part, that is not true, as Bitcoin will usually rise and fall with stocks and, to a lesser extent, bonds. Notably, although its bond correlation is never very high, it is almost never negative, implying that it is potentially not an inflation hedge (given bonds are negatively exposed to inflation).

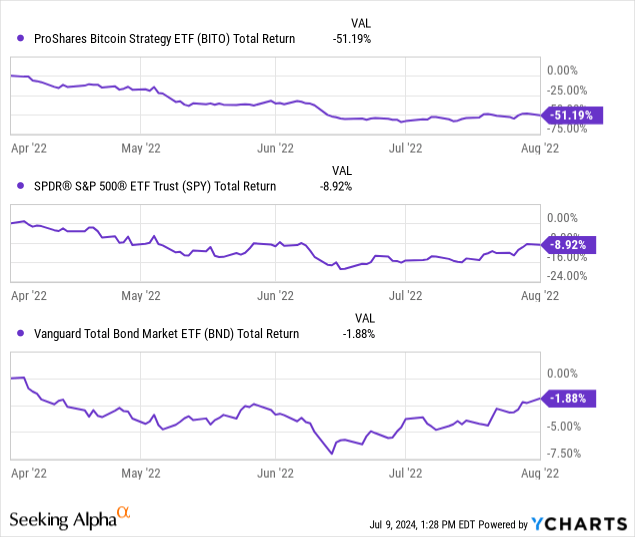

On a shorter-term basis, BITO is not so highly correlated to stocks and bonds that investors may notice. Indeed, some exposure to BITO would reduce overall portfolio volatility on a day-to-day basis, given its correlation is usually below 0.5. However, during market crashes, or periods of considerable volatility, it is often the case that correlations rise, causing exposure to increase when it is most problematic. For example, during the summer of 2022, which saw an increased interest rate outlook amid inflation concerns, we saw notable declines in Bitcoin, which was well-mirrored in the S&P 500 and bond market. See below:

Of course, this is just one example, but investors may want to remember it. During low volatility periods, it may seem that BITO and Bitcoin are not highly exposed to general market risk. However, when volatility increases, and people are looking to sell virtually anything, Bitcoin seems to be among the things people wish to sell. Again, that implies that it is a speculative asset, not a hedge, and may crash during a period of negative stock or bond market activity.

Indeed, the recent declines in Bitcoin, mirrored in BITO, potentially indicate an increase in general financial market risk. Those who’ve read my articles likely know that I see markets as primarily liquidity-driven (cash, bank lending, Fed QE/QT) and secondarily driven by fundamentals (earnings, economy, etc.) Over recent years, most aspects of the US and global economy have stagnated, with some growing (technology) and other sectors declining (manufacturing). Still, most stocks, huge technology stocks have seen their best performance. To me, that is because the financial system has had excess liquidity coming out of the COVID stimulus and QE efforts, most of which are now burned up amid QT.

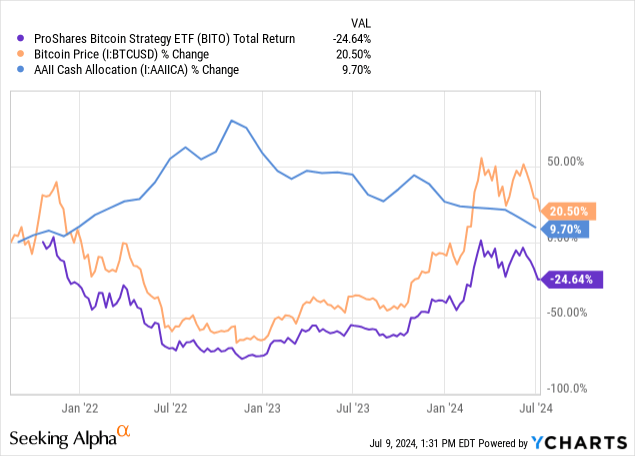

This pattern is mirrored by the relationship between Bitcoin, BITO, and individual investor cash allocations. For example, as rates were rising in 2022, many individual investors flocked to cash to take advantage of higher rates and reduce exposure to the usual economic risk that comes from higher rates. We saw Bitcoin crash during that “negative individual investor liquidity” period. However, that led to a buildup in cash allocations, which have since been redeployed into (in my view) primarily speculative assets from those looking for abnormal short-term gains. No surprise, Bitcoin and BITO have likely been among those. See below:

Note that this shows the change in cash allocations from the baseline. The average individual investor cash allocation level from AAII surveys is 15% today, which is the typical cyclical minimum. Usually, when cash allocations are this low, markets tend to decline or stagnate as there is insufficient sideline cash to deploy.

Many broader economic and monetary factors point to less liquidity for speculative instruments. Of course, the Fed is effectively “deleting” money through its slow QT program, bank deposits are stuck (capping lending), and personal household savings are very low (due to rising living costs). Thus, the potential sideline cash that could be deployed into Bitcoin is far lower than it has been over most of the past two years or perhaps even in Bitcoin’s history (until recently, during periods of extreme money supply growth). The only area of decent liquidity is foreign banks with US cash. I suspect that is due to more significant monetary issues in countries like Japan. However, I do not believe the potential return of overseas US dollars is sufficient to improve the overall US financial market liquidity decline.

When investors treat cash as valuable during periods of lower liquidity, we usually see overvalued financial assets decline. Conversely, periods of low interest rates or excess liquidity growth often cause some financial assets to become overvalued. From that view, I believe Bitcoin has been an area where investors with extra cash have speculatively deployed money and will thus withdraw that money first as liquidity falls back into short supply.

Although the Fed may cut rates, that will likely require a continued rise in unemployment. I believe there is very strong evidence to suggest that we’re seeing the beginnings of a much larger increase in unemployment. To me, the liquidity demands of higher unemployment would be far greater than any added supply from rate cuts. However, a return of QE could provide enough liquidity that Bitcoin and BITO may benefit. That said, I suspect that we will not see QE return until/unless stocks, bonds, and Bitcoin are far lower.

Does BITO Face Added Liquidity Risk?

Previously, one issue I saw with BITO was its exposure to the Bitcoin futures market. As I discussed, BITO owns most of the Bitcoin futures market, so if Bitcoin crashes, there may not be sufficient counterparties to the ETF. One issue is that it may have poor tax exposure because it has to occasionally sell futures and realize gains, distributing them as a cash payment. Again, BITO does not have a 41% yield, as that “yield” represents the distribution of its gains on futures, which are likely to be taxed at the short-term rate because the holding period will generally be low.

Those curious should research this issue, though that is what I surmise based on the research of others. However, from an overall efficiency standpoint, I am sure that owning Bitcoin outright is the best option for taxation issues (given your holding period is over a year), counterparty liquidity, and avoidance of BITO’s 95 bps expense ratio.

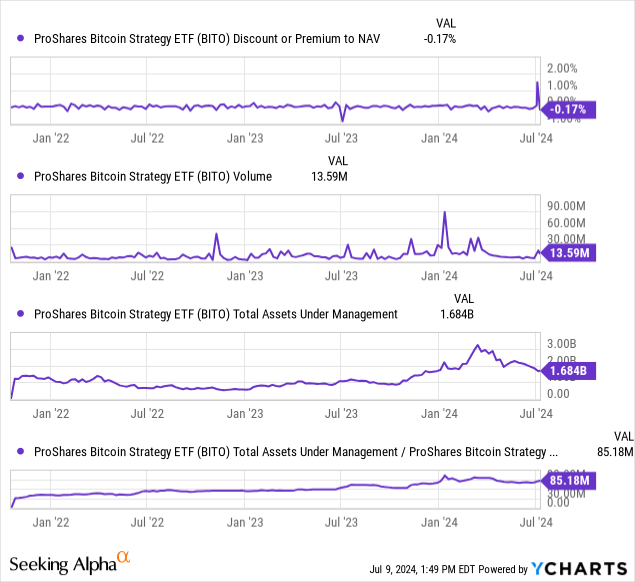

BITO’s potential counterparty liquidity issues were highlighted recently as its premium shot up during increased Bitcoin volatility. See below:

Realistically, the counterpart risk to BITO is a short-term problem. It may be that if you’re looking to sell BITO during a crash (the same day or the same week), there is a chance that BITO has an odd premium or discount that could be pretty large. To me, this risk is higher today because BITO has become very popular, as seen in its outstanding share (measured by AUM/price in the lowest chart). Again, BITO should always settle very close to Bitcoin’s spot price, but I would not want to sell the fund during a period where many others are as well since that is likelier to see a greater spread between its NAV and price. Still, that spread could be positive, potentially making it a benefit.

The Bottom Line

Overall, I downgrade my view on BITO from bearish to very bearish, with my expectation that Bitcoin has reached a cyclical peak and is becoming more firm. Since January, we’ve seen the necessary continued deterioration in total financial market liquidity drivers, such that there is insufficient “sideline cash” for Bitcoin to continue to rise.

Again, while I like some cryptocurrencies, I see zero fundamental value to Bitcoin and believe it is a waste of increasingly scarce electricity resources. So then, for me, Bitcoin relies on the “Greater Fool Theory.” In other words, I think having a bullish view of Bitcoin is entirely valid if you feel it may rise due to speculative momentum. However, considering its fundamentals as a cryptocurrency, its correlations with other asset classes, and market liquidity, it is, to me, very clear that it is only driven by excess liquidity. BITO is where you park money you don’t need, hoping it may rise, but not an investment that causes proper (economic) capital growth, as seen in most stocks.

To that end, I think BITO should decline at a faster pace because I believe financial market excess liquidity is drying up much faster and could evaporate if we see a large upward swing to unemployment. If the Fed is swift to cut rates and pursue QE, Bitcoin may stand to benefit. Of course, the Fed is, in my view, almost always too late. However, I expect that gold and silver (in particular) would benefit the most in that scenario. It is worth pointing out that silver and gold may also decline during market shocks, but not likely to the same extent as Bitcoin, which behaves more similarly to the stock market than the physical commodities.

Would I short BITO or Bitcoin today? Perhaps, but not necessarily. Over the first half of 2024, I’ve shifted from the view that “Bitcoin may peak soon” to “Bitcoin has likely peaked.” To me, it remains unclear how considerable Bitcoin’s overall downside is. I feel that Bitcoin may be due for a record decline because many may need to sell it if unemployment spikes in a traditional recession. Bitcoin remains untested in a conventional recession, given the 2020 recession was driven by external circumstances and was met with extreme liquidity stimulus.

I guess that Bitcoin may perceptively become “BitCon” as in a “con” in a 2000-like market crash, but that is speculative. Personally, I am not going to place a short on my guesses, as I feel there are other assets where short-selling is less risky. So, I may bet against BITO today. However, I would only do so with a small allocation since its downside is unclear. We could still see a resurgence in bullish speculative activity. However, I believe the odds of that are increasingly low.

Lastly, it may be that my belief that Bitcoin has no value as an alternative to fiat currency is proven incorrect. Still, again, in a world where electricity and energy prices are rising, I cannot see how Bitcoin could be a long-term viable currency alternative where many cryptocurrencies do not require so much energy per transaction.