Markets

Coinbase and Robinhood: JMP chooses the best crypto stocks to buy

Bitcoin’s fourth halving happened quietly last month, when the 840,000th block was mined. Despite the official increase in scarcity, BTC prices have remained relatively stable. This stability could present new opportunities for potential crypto investors. Historically, halving events are accompanied by price increases, as the number of coins awarded for each mined block decreases.

However, the unregulated nature of the cryptocurrency market can be intimidating. However, this should not deter potential investors. Those who want to capitalize on the crypto market but are hesitant to purchase the currencies directly can consider investing in crypto-related stocks. These stocks are regulated, thereby reducing risk for investors while maintaining investment quality.

Covering crypto for investment bank JMP, 5-star analyst Devin Ryan gives strong opinions on the best crypto stocks to buy in the current environment. Ryan looks at Coinbase (NASDAQ:COIN) and Robinhood (NASDAQ:HOOD), two big names in the crypto trading world, and his opinions are worth a closer look.

We used the TipRanks database to find out what the rest of the street has to say about these two picks. Let’s go.

Global Coinbase

We’ll start with Coinbase, one of the leading digital cryptocurrency exchanges. The company operates an online platform and cryptocurrency wallet, accessible from PCs and mobile devices, offering trading on most major cryptocurrencies. Users can buy, sell and trade Bitcoin, Ethereum, Dogecoin – 248 cryptos in total. Coinbase makes its app interface simple and intuitive to use, to make the trading process as simple as possible – and to apply it outside of the digital currency niche.

The service has proven popular and Coinbase is available in over 100 countries. The app hosts a quarterly volume of approximately $312 billion and the company supports its trading with over $348 billion in total listed assets. Coinbase also works to improve trust in the crypto space and is committed to upholding the best practices of traditional financial services companies.

The Coinbase stock price tends to follow the price of Bitcoin, and when the flagship cryptocurrency began to gain earlier this year, COIN shares also saw a sharp rise. Increased investor interest in the crypto platform company has translated into strong gains for the stock, which is up approximately 220% over the past 12 months. The company now has a market capitalization of nearly $49 billion.

The company’s financial results were strong in the first quarter of this year. Coinbase reported total revenue of just over $1.6 billion, beating forecasts by $300 million and growing 112% year over year. Ultimately, Coinbase delivered EPS of $4.40, a sharp turnaround from the net EPS loss of 34 cents recorded in 1Q23 – and beating forecasts of $3.33 per share.

Coinbase has attracted the attention of analyst Devin Ryan primarily for its growth potential. The analyst, ranked 21st overall by TipRanks, writes of the company: “While growth from here is not linear, we believe it is becoming increasingly clear to the market that Coinbase built one of the most holistic on-ramps in the world. the digital asset economy and for virtually all types of users, including retailers (for many use cases beyond commerce), institutions, merchants, developers (and more). Simply put, this business is evolving into much more than just a marketplace for buying and selling digital assets, which has been our consistent thesis.

Looking ahead, Ryan goes on to describe what specifically is encouraging Coinbase stock at the moment, saying: “We believe investors should size their positions by viewing the stock as a higher risk proposition given the volatility inherent to crypto markets and also the ongoing uncertainty around. regulatory and legislative issues. That said, we view the risk/reward opportunity as attractive…”

Taken together, these comments support Ryan’s Outperform (i.e. Buy) rating on Coinbase shares, and his $320 price target shows his confidence in ~61% upside potential. for the coming year. (To see Ryan’s track record, Click here)

Overall, Coinbase earns a Moderate Buy consensus rating from Wall Street analysts, based on 21 recent reviews that break down into 9 Buys, 9 Holds, and 3 Sells. Shares are trading at $199.17, and their average price target of $244.37 suggests a one-year upside of around 23%. (See Coinbase Stock Forecast)

Robinhood Markets

The second stock we’ll look at is online financial services company Robinhood. Robinhood has been offering commission-free trading on its platform, on stocks, ETFs, IRAs – and cryptocurrencies since 2022. Robinhood launched its mobile app in 2015 and quickly became popular with young investors.

Robinhood offers a number of benefits to young investors new to trading markets. The platform allows users to trade from as little as one dollar and also makes funds available through the Robinhood Gold Card or Crypto Wallet. It’s all part of Robinhood’s self-proclaimed mission to democratize finance for everyone. Some numbers show the company’s progress in this direction: It has 24 million funded customers as of April 30 and claims $123 billion in assets under custody.

The popularity of the Robinhood app and its popularity as a cryptocurrency trading platform is reflected in the company’s stock performance; over the past 12 months, the stock is up about 111%. The stock posted these gains despite choppy trading and a few losing sessions in recent weeks.

Turning to the company’s financial results, we note that the 1Q24 report, the most recent, presents several record numbers. Quarterly revenue was $618 million, up 40% year over year, hitting a record for the company. The end result was another record, with GAAP EPS reported at 18 cents per share. Revenue was $63 million above forecast and EPS was 12 cents per share. These figures were bolstered by record net deposits of $11.2 billion.

Record performance and strong annual growth have JMP’s Devin Ryan paying attention to Robinhood and taking a more bullish stance than the Street in general.

“We believe Robinhood can continue to deliver better-than-expected growth and profitability, all supportive of valuation… With the re-acceleration of revenue growth, coupled with management’s focus on expenses, we We estimate that the company should be able to deliver an average profit growth of +30% in the coming years, with significant room for improvement before the business model reaches a more “mature” state. At the same time, Robinhood’s financial stability has never been better, with liquidity and investments exceeding $5 billion, or about a third of the total market capitalization,” Ryan said.

Regarding his own results, Ryan says: “Based on our growth projections for the next few years, we view the valuation as quite compelling…”

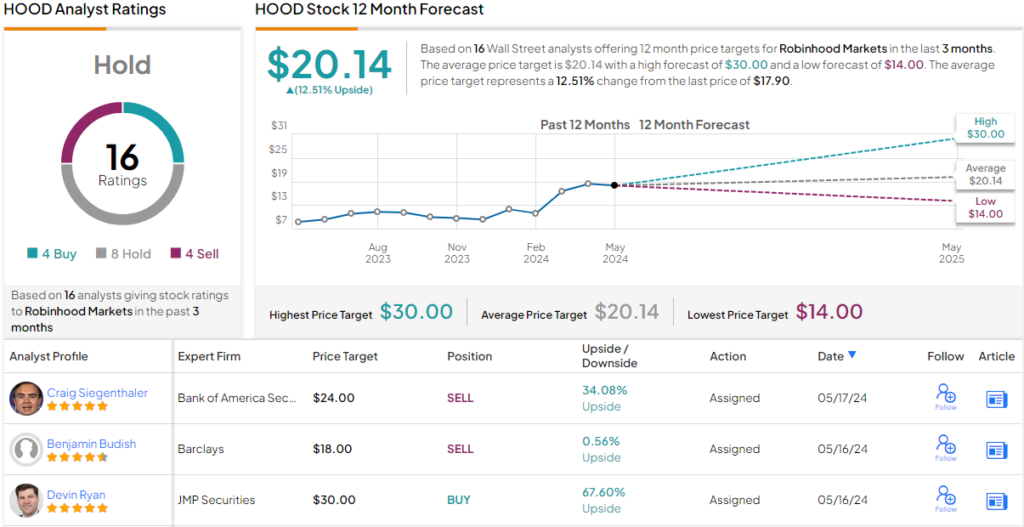

Quantifying his bullish stance, Ryan gives an Outperform (i.e. Buy) rating to HOOD shares, and he sets a $30 price target that suggests a stock gain of around 68% at during the coming year.

This is the bullish position. The broader street view puts HOOD on hold, based on 16 reviews including 4 to buy, 8 to hold and 4 to sell. Robinhood shares are selling for $17.90, and the stock’s average price target of $20.14 implies a 12-month upside of 12.5%. (See Robinhood Stock Forecast)

To find great ideas for trading stocks at attractive valuations, visit TipRanks. Best Stocks to Buya tool that brings together all the information about stocks from TipRanks.

Disclaimer: The opinions expressed in this article are solely those of the analyst featured. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.