News

Could financial weakness mean the market will correct its share price?

Most readers will already know that SLP Resources Berhad (KLSE:SLP) shares have risen significantly by 9.5% over the past month. However, in this article, we decided to focus on its weak fundamentals, since a company’s long-term financial performance is what ultimately dictates market outcomes. Specifically, we decided to study SLP Berhad’s Resources ROE in this article.

ROE or return on equity is a useful tool for evaluating how effectively a company can generate returns on the investment it has received from its shareholders. In short, ROE shows the profit that each dollar generates in relation to its shareholders’ investments.

See our latest analysis for SLP Resources Berhad

How to calculate return on equity?

O formula for return on equity It is:

Return on Equity = Net Profit (from continuing operations) ÷ Equity

Therefore, based on the above formula, SLP Resources Berhad’s ROE is:

6.5% = RM13 million ÷ RM194 million (Based on trailing twelve months to March 2024).

The ‘return’ is the annual profit. One way to conceptualize this is that for every MYR1 of share capital it has, the company made MYR0.06 in profit.

What is the relationship between ROE and earnings growth?

So far, we’ve learned that ROE is a measure of a company’s profitability. Based on how much of its profits the company chooses to reinvest or “retain”, we can then assess a company’s future ability to generate profits. Assuming everything else remains unchanged, the higher the ROE and profit retention, the higher a company’s growth rate compared to companies that don’t necessarily exhibit these characteristics.

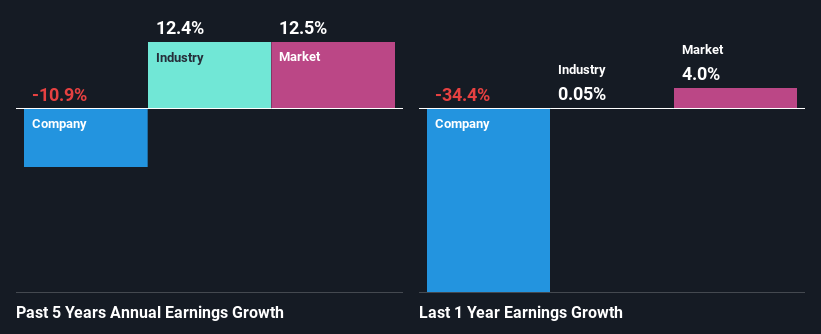

SLP Resources Berhad Earnings Growth and ROE of 6.5%

At first glance, there isn’t much to say about SLP Resources Berhad’s ROE. However, its ROE is similar to the industry average of 8.0%, so we wouldn’t write off the company entirely. That said, SLP Resources Berhad’s five-year net profit decline rate was 11%. Keep in mind that the company’s ROE is a bit low to begin with. Therefore, the drop in income could also be a result of this.

That being said, we compared SLP Resources Berhad’s performance to the industry and were concerned when we discovered that although the company decreased its profits, the industry grew its profits at a rate of 12% over the same 5-year period.

past profit growth

Earnings growth is an important factor in stock valuation. The investor should attempt to establish whether the expected growth or decline in earnings, whatever the case may be, is priced in. This will help you determine whether the stock’s future looks promising or ominous. Is SLP Resources Berhad fairly valued compared to other companies? Those 3 assessment measures can help you decide.

The story continues

Is SLP Resources Berhad making efficient use of its profits?

SLP Resources Berhad has a high three-year average payout ratio of 98% (i.e. it is retaining 1.9% of its profits). This suggests that the company is paying out most of its profits as dividends to its shareholders. This goes some way to explaining why their profits have been declining. With only very little to reinvest in the business, earnings growth is far from likely. Our risk dashboard it must have the 2 risks we identified for SLP Resources Berhad.

Furthermore, SLP Resources Berhad has been paying dividends for at least ten years or more, suggesting that management must have realized that shareholders prefer dividends to earnings growth. Our latest analyst data shows that the company’s future payout ratio over the next three years is expected to be approximately 82%. Regardless, SLP Resources Berhad’s future ROE is expected to increase to 10%, despite there not being many changes expected in its payout ratio.

Conclusion

Overall, we would be extremely cautious before making any decisions about SLP Resources Berhad. In particular, its ROE is a huge disappointment, not to mention the lack of adequate reinvestment in the business. As a result, its earnings growth was also quite disappointing. That said, analyzing current analyst estimates, we find that the company’s earnings growth rate is expected to see a huge improvement. To learn more about the company’s future earnings growth forecasts, take a look at this free report on analyst forecasts for the company to find out more.

Do you have feedback on this article? Worried about the content? Get in touch with us directly. Alternatively, email the editorial team (at) Simplywallst.com.

This Simply Wall St article is general in nature. We provide commentary based on historical data and analyst forecasts using only an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take into account your objectives or financial situation. Our goal is to bring you long-term focused analysis driven by fundamental data. Please note that our analysis may not take into account the latest price-sensitive company announcements or qualitative materials. Simply Wall St has no position in any of the stocks mentioned.