News

Financials Could Boost Diversified Royalty Corp. Stock Price (TSE: DIV)?

Shares of Diversified Royalty (TSE:DIV) were roughly flat last week. However, attentive investors would likely pay more attention to the stock, as the company’s fundamentals could add more to the story, considering that long-term financials are usually what drive market prices. Specifically, we decided to study Diverse royalty ROE in this article.

ROE or return on equity is a useful tool for evaluating how effectively a company can generate returns on the investment it has received from its shareholders. In short, ROE shows the profit that each dollar generates in relation to its shareholders’ investments.

See our latest analysis for Diversified Royalties

How is ROE calculated?

O formula for ROE It is:

Return on Equity = Net Profit (from continuing operations) ÷ Equity

Therefore, based on the above formula, the ROE for Diversified Royalty is:

11% = CA$33m ÷ CA$290m (Based on trailing twelve months to March 2024).

The ‘return’ refers to a company’s profits over the last year. This means that for every CA$1 of shareholders’ equity, the company generated CA$0.11 in profit.

Why is ROE important for earnings growth?

So far, we have learned that ROE measures how efficiently a company is generating its profits. Based on how much of its profits the company chooses to reinvest or “retain”, we can then assess a company’s future ability to generate profits. Generally speaking, other things being equal, companies with a high return on equity and profit retention have a higher growth rate than companies that do not share these attributes.

A side-by-side comparison of diversified royalty earnings growth and 11% ROE

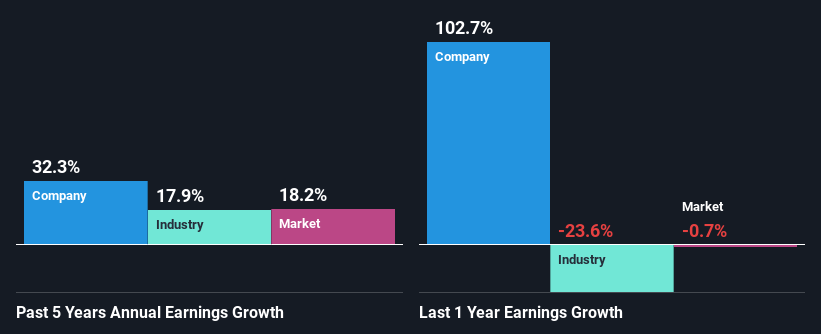

For starters, Diverse Royals appears to have a respectable ROE. Even when compared to the industry average of 9.8%, the company’s ROE looks pretty decent. Consequently, this likely laid the foundation for the impressive 32% net income growth seen over the past five years by Diversified Royalty. We think there could also be other factors at play here. For example, the company has a low payout ratio or is being run efficiently.

Next, when comparing this to industry net profit growth, we find that Diversified Royalty’s growth is quite high when compared to the industry average growth of 18% over the same period, which is great to see.

past profit growth

Earnings growth is an important factor in stock valuation. The investor should attempt to establish whether the expected growth or decline in earnings, whatever the case may be, is priced in. This helps you determine whether the stock is poised for a bright or bleak future. How much is DIV worth today? O intrinsic value infographic in our free research report helps visualize whether the DIV is currently mispriced by the market.

The story continues

Are the diverse royals making efficient use of their profits?

Diversified Royalty’s very high three-year average payout ratio of 151% suggests the company is paying more to its shareholders than it is earning. Despite this, the company’s profit grew significantly as we saw above. That said, it may be worth keeping an eye on the high payout ratio as this represents a huge risk. To learn about the 3 risks we identified for Diversified Royalty, visit our risk panel for free.

Additionally, Diversified Royalty has been paying dividends for at least ten years or more. This shows that the company is committed to sharing profits with its shareholders.

Conclusion

Altogether, it appears that Diversified Royalty has some positive aspects to its business. Specifically, its high ROE, which likely led to earnings growth. Keep in mind that the company reinvests little or none of its profits, which means investors are not necessarily reaping the full benefits of the high rate of return. So far, we have only touched the surface of the company’s past performance, analyzing its fundamentals. For more information on Diversified Royalty’s past earnings growth, check out this visualization of past earnings, revenue and cash flows.

Do you have feedback on this article? Worried about the content? Get in touch with us directly. Alternatively, email the editorial team (at) Simplywallst.com.

This Simply Wall St article is general in nature. We provide commentary based on historical data and analyst forecasts using only an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take into account your objectives or your financial situation. Our goal is to bring you long-term focused analysis driven by fundamental data. Please note that our analysis may not take into account the latest price-sensitive company announcements or qualitative materials. Simply Wall St has no position in any of the stocks mentioned.