News

Here’s Why Ulta Beauty Is One of the Smartest Stocks to Buy Dip

Shares of the cosmetics retail chain Ultra Beauty (NASDAQ: ULTA) are down more than 30% from their all-time highs. But this is not a business in decline. And it’s very easy to prove.

Ulta Beauty has no long-term debt as of February 2024. How to invest big Peter Lynch used to say, “It’s very difficult to go bankrupt when you don’t have any debt.” To this I will add that it is even more difficult to go bankrupt when a company is also profitable. And Ulta is very profitable with a operating profit margin of 15% in its 2023 fiscal year.

To reiterate, the stock is down. But there’s a reason for this drop: At a recent investor conference, management said fiscal 2024 started below its expectations. Consequently, it believes it will present numbers at the lower end of its financial guidance.

I believe this is clearly a classic case of investors overreacting to the news. After all, Ulta Beauty didn’t follow its guidance. On the contrary, the administration said it would meet its financial guidance, albeit at the lower end.

For perspective, the lower end of its fiscal 2024 net sales guidance is $11.7 billion. That’s still a 4% annual increase.

The company has a clean balance sheet, is profitable and continues to grow at a modest pace – as I said, it’s easy to establish that this is not a business in decline. But with stocks down, investors now face one of two likely outcomes. And both are good for shareholders.

Scenario #1: Ulta Beauty returns to normal

Ulta Beauty shares currently have a price-to-sales (P/S) ratio of 1.7, which is very cheap. Looking at its 10-year chart, it traded with a P/S as high as 4 and as low as 1. But it had an average P/S rating of 2.6.

ULTA PS Ratio Chart

Let’s say investors slowly realize that stocks are cheap and fears are exaggerated. If investor demand increases and the shares return to a normal valuation, they could appreciate by around 50%. That’s a good deal.

Plus, aside from the stock market crash caused by the pandemic, Ulta Beauty has never been cheaper in the last decade. So it’s hard to imagine the stock has much more downside today. Bad expectations are already reflected in the cheap price.

In short, the stock could have little downside, with a 50% upside opportunity.

Scenario #2: Ulta Beauty Stock Remains Cheap

It’s also possible that the stock could become cheap or even become cheaper (even though I think that’s unlikely). This would be counterintuitively good for patient long-term investors as well.

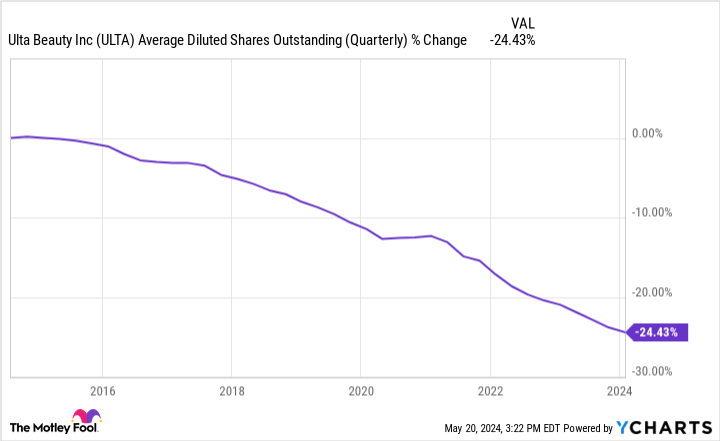

Over the past decade, Ulta Beauty management has spent nearly $6 billion repurchasing its shares. This increases the value per share for those who own them.

The story continues

ULTA Chart Average number of diluted shares outstanding (quarterly)

Given that it’s a profitable business with a track record of returning money to shareholders, Ulta Beauty will likely continue repurchasing shares at a generous rate. The problem is that when stocks are cheap, as they are now, a stock buyback program gets more bang for your buck.

Why it’s a win-win situation

I admit, it’s possible that Ulta Beauty will lay an egg when it reports financial results for the first quarter of fiscal 2024 on May 30. After all, the aforementioned investor conference took place just weeks after management gave financial guidance. Something has changed in a short time and it is possible that things have gotten even worse at a rapid pace.

However, I consider it more likely that management only noticed a modest temporary slowdown in cosmetics spending; This is not a permanent separation of consumers from their products and services.

If this is just the normal ebb and flow of business, then the company is still well prepared for the long term – which still makes it a quality investment candidate. And since shares are cheap, either the valuation will recover or management may repurchase more shares. Either way, Ulta Beauty shareholders win, making this a smart stock for patient investors to buy the dip now.

Should you invest $1,000 in Ulta Beauty right now?

Before buying Ulta Beauty stock, consider the following:

The Motley Fool Stock Advisor analyst team just identified what they believe is the 10 best stocks for investors to buy now… and Ulta Beauty wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia I made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you would have $635,982!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular analyst updates, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of the S&P 500 since 2002*.

*Stock Advisor returns May 13, 2024

Jon Quast has no position in any of the stocks mentioned. The Motley Fool has positions and recommends Ulta Beauty. The motley fool has a disclosure policy.

Here’s Why Ulta Beauty Is One of the Smartest Stocks to Buy Dip was originally published by The Motley Fool