News

Is the strong financial outlook the force driving momentum in Devon Energy Corporation (NYSE:DVN) stock?

Devon Energy (NYSE:DVN) has had a great run on the stock market, with its shares rising a significant 11% over the past three months. Given that the market rewards strong financials over the long term, we wonder if that will be the case in this case. Specifically, we decided to study Devon Energy ROE in this article.

Return on equity or ROE is a test of how effectively a company is growing its value and managing investors’ money. Put another way, it reveals the company’s success in transforming shareholder investments into profits.

See our latest analysis for Devon Energy

How to calculate return on equity?

O formula for return on equity It is:

Return on Equity = Net Profit (from continuing operations) ÷ Equity

Therefore, based on the above formula, Devon Energy’s ROE is:

27% = $3.4 billion ÷ $12 billion (based on trailing twelve months to March 2024).

The ‘return’ is the annual profit. So, this means that for every US$1 of investment by its shareholders, the company generates a profit of US$0.27.

What does ROE have to do with earnings growth?

We have already established that ROE serves as an efficient profit-generating indicator for a company’s future earnings. Depending on how much of these profits the company reinvests or “retains”, and how effectively it does so, we will then be able to assess a company’s earnings growth potential. Assuming everything else remains unchanged, the higher the ROE and profit retention, the higher a company’s growth rate compared to companies that don’t necessarily exhibit these characteristics.

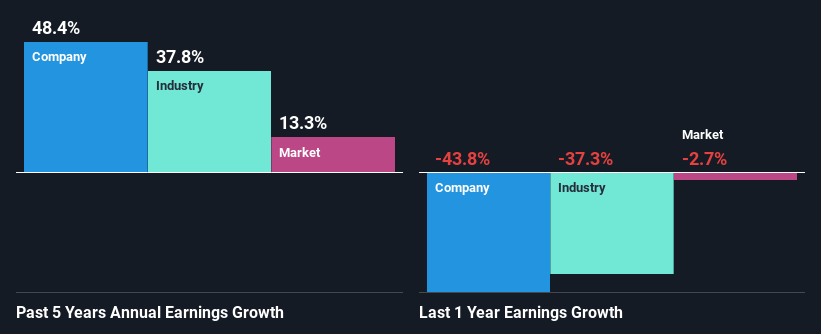

A side-by-side comparison of Devon Energy’s earnings growth and 27% ROE

Firstly, we like that Devon Energy has an impressive ROE. Secondly, even when compared to the industry average of 18%, the company’s ROE is quite impressive. As a result, Devon Energy’s exceptional 48% net profit growth seen over the past five years comes as no surprise.

Next, when comparing this to the industry’s net profit growth, we find that Devon Energy’s growth is quite high when compared to the industry average growth of 38% over the same period, which is great to see.

past profit growth

The basis for adding value to a company is, to a large extent, linked to the growth of its profits. What investors need to determine next is whether the expected earnings growth, or lack thereof, is already factored into the stock price. This will help them determine whether the stock’s future looks promising or ominous. Is DVN valued fairly? That infographic about the intrinsic value of the company It has everything you need to know.

The story continues

Is Devon Energy using its retained earnings effectively?

The high three-year average payout ratio of 50% (implying it only keeps 50% of the profits) for Devon Energy suggests that the company’s growth has not actually been hampered, despite returning most of the profits to its shareholders.

Furthermore, Devon Energy has been paying dividends for at least ten years or more. This shows that the company is committed to sharing profits with its shareholders. By studying the latest analyst consensus data, we found that the company’s future payout ratio is expected to fall to 27% over the next three years. Regardless, Devon Energy’s future ROE is forecast to decline to 20% despite the anticipated reduction in the payout ratio. We believe there likely could be other factors that could be driving the anticipated decline in the company’s ROE.

Conclusion

Overall, we feel that Devon Energy’s performance has been quite good. In particular, its high ROE is quite noteworthy and also the likely explanation behind its considerable earnings growth. Even so, the company retains a small part of its profits. Which means the company managed to increase its profits despite this, which isn’t so bad. That said, in studying current analyst estimates, we were concerned to see that while the company has grown its earnings in the past, analysts expect its earnings to decline in the future. To learn more about the latest analyst forecasts for the company, check out this visualization of analyst forecasts for the company.

Do you have feedback on this article? Worried about the content? Get in touch with us directly. Alternatively, email the editorial team (at) Simplywallst.com.

This Simply Wall St article is general in nature. We provide commentary based on historical data and analyst forecasts using only an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take into account your objectives or your financial situation. Our goal is to bring you long-term focused analysis driven by fundamental data. Please note that our analysis may not take into account the latest price-sensitive company announcements or qualitative materials. Simply Wall St has no position in any of the stocks mentioned.