News

The weak financial outlook appears to be hurting Vector Limited (NZSE:VCT) shares

Vector (NZSE:VCT) has had a tough three months, with its share price falling 6.7%. Given that stock prices are typically driven by a company’s long-term fundamentals, which in this case appear quite weak, we decided to study the company’s key financial indicators. Specifically, we decided to study Vector ROE in this article.

Return on equity or ROE is a fundamental measure used to evaluate how efficiently a company’s management is utilizing the company’s capital. Put another way, it reveals the company’s success in transforming shareholder investments into profits.

See our latest analysis for Vector

How do you calculate return on equity?

O formula for return on equity It is:

Return on Equity = Net Profit (from continuing operations) ÷ Equity

Therefore, based on the above formula, the ROE for Vector is:

1.9% = NZ$71m ÷ NZ$3.8b (Based on trailing twelve months to December 2023).

The ‘return’ is the revenue the company made in the last year. This means that for every NZ$1 of equity, the company generated NZ$0.02 in profit.

What is the relationship between ROE and earnings growth?

We have already established that ROE serves as an efficient profit-generating indicator for a company’s future earnings. Depending on how much of these profits the company reinvests or “retains”, and how effectively it does so, we will then be able to assess a company’s earnings growth potential. Assuming everything else is equal, companies that have a higher return on equity and higher profit retention are generally those that have a higher growth rate when compared to companies that do not have the same characteristics.

Vector earnings growth and ROE of 1.9%

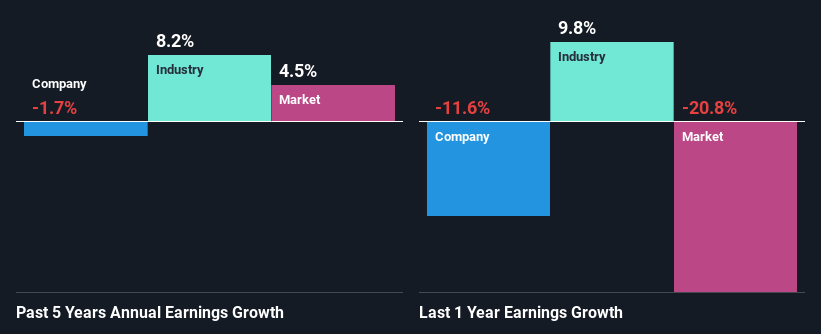

It’s hard to argue that Vector’s ROE is very good on its own. Even compared to the industry average ROE of 9.5%, the company’s ROE is quite underwhelming. Therefore, Vector’s stable profits over the last five years can possibly be explained by low ROE, among other factors.

Next, comparing with the industry’s net profit growth, we find that the industry has increased its profit by 8.2% in recent years.

past profit growth

The basis for adding value to a company is, to a large extent, linked to the growth of its profits. What investors need to determine next is whether the expected earnings growth, or lack thereof, is already factored into the stock price. This will help them determine whether the stock’s future looks promising or ominous. Is the ATV valued fairly? That infographic about the intrinsic value of the company It has everything you need to know.

The story continues

Is Vector making efficient use of its profits?

Vector’s very high three-year average payout ratio of 146% suggests the company is paying its shareholders more than it earns. This goes some way to explaining the insignificant earnings growth seen by Vector. Paying a dividend higher than declared profits is not a sustainable measure. This is indicative of risk. To learn about the 3 risks we identified for Vector, visit our risk panel for free.

Furthermore, Vector has been paying dividends for at least ten years or more, suggesting that management must have realized that shareholders prefer dividends to earnings growth. By studying the latest analyst consensus data, we found that the company’s future payout ratio is expected to fall to 77% over the next three years. Thus, the expected drop in the payout ratio explains the expected increase in the company’s ROE to 6.7% in the same period.

Conclusion

In total, we would have to think long and hard before deciding on any investment action regarding Vector. Specifically, it has demonstrated quite poor performance when it comes to earnings growth, and a weak ROE and similarly low reinvestment rate appear to be the reason behind this inadequate performance. That said, analyzing current analyst estimates, we find that the company’s earnings growth rate is expected to see a huge improvement. To learn more about the latest analyst forecasts for the company, check out this visualization of analyst forecasts for the company.

Do you have feedback on this article? Worried about the content? Get in touch with us directly. Alternatively, email the editorial team (at) Simplywallst.com.

This Simply Wall St article is general in nature. We provide commentary based on historical data and analyst forecasts using only an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take into account your objectives or your financial situation. Our goal is to bring you long-term focused analysis driven by fundamental data. Please note that our analysis may not take into account the latest price-sensitive company announcements or qualitative materials. Simply Wall St has no position in any of the stocks mentioned.